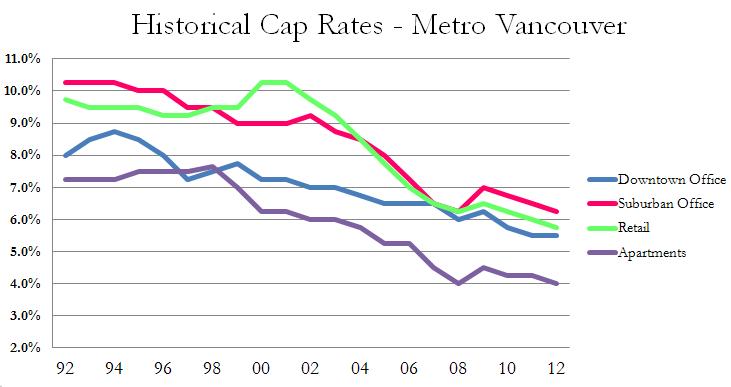

Cap Rate Compression: How Much Longer Can it Last?

Over the past few years, a significant proportion of the increasing value of commercial real estate in Vancouver has been attributed to declining capitalization rates. This so-called “cap-rate compression” has been evidenced by seemingly perpetual price appreciation in Vancouver throughout the past several years, with only a small blip in the markets in late 2008 and early 2009. Since that time, cap rates have followed the march of the bond market.

When will we witness the end of declining capitalization rates? Logic would dictate that this trend cannot be sustained; however, with continued low bond yields, debt financing can continue to be characterized as ‘cheap’, and many investors will continue to be attracted to Vancouver’s overall low-risk profile.

Yields on 5-year bonds are forecast to increase approximately 50 basis points by the end of 2013. This may have an impact on lower-tier properties and those in secondary markets, where average yields may increase by as much as 50-100 BPS. On the other hand, with continued global economic uncertainty, Vancouver may benefit from sustained low interest rates and a ‘safe’ outlook, particularly in core areas where there remains high barriers to new supply.