There are a whopping fifteen rezoning applications going to City of Vancouver Council next week, spanning neighbourhoods from Downtown to the Fraser River waterfront. Here’s a rundown of what’s being considered:

2806–2890 East Broadway, 2813–2881 East 10th Avenue & 2528–2580 Kaslo Street

Applicant: Sightline Properties

A 26-lot land assembly just north of Renfrew SkyTrain Station is proposed for four mixed-use towers ranging from 39 to 45 storeys, totalling 1,959 units (1,386 strata and 573 rental, with 20% of rental floor area at below-market rates), plus ground-floor retail and a 73-space private childcare facility. Density is 10.5 FSR. Application prepared by Arcadis.

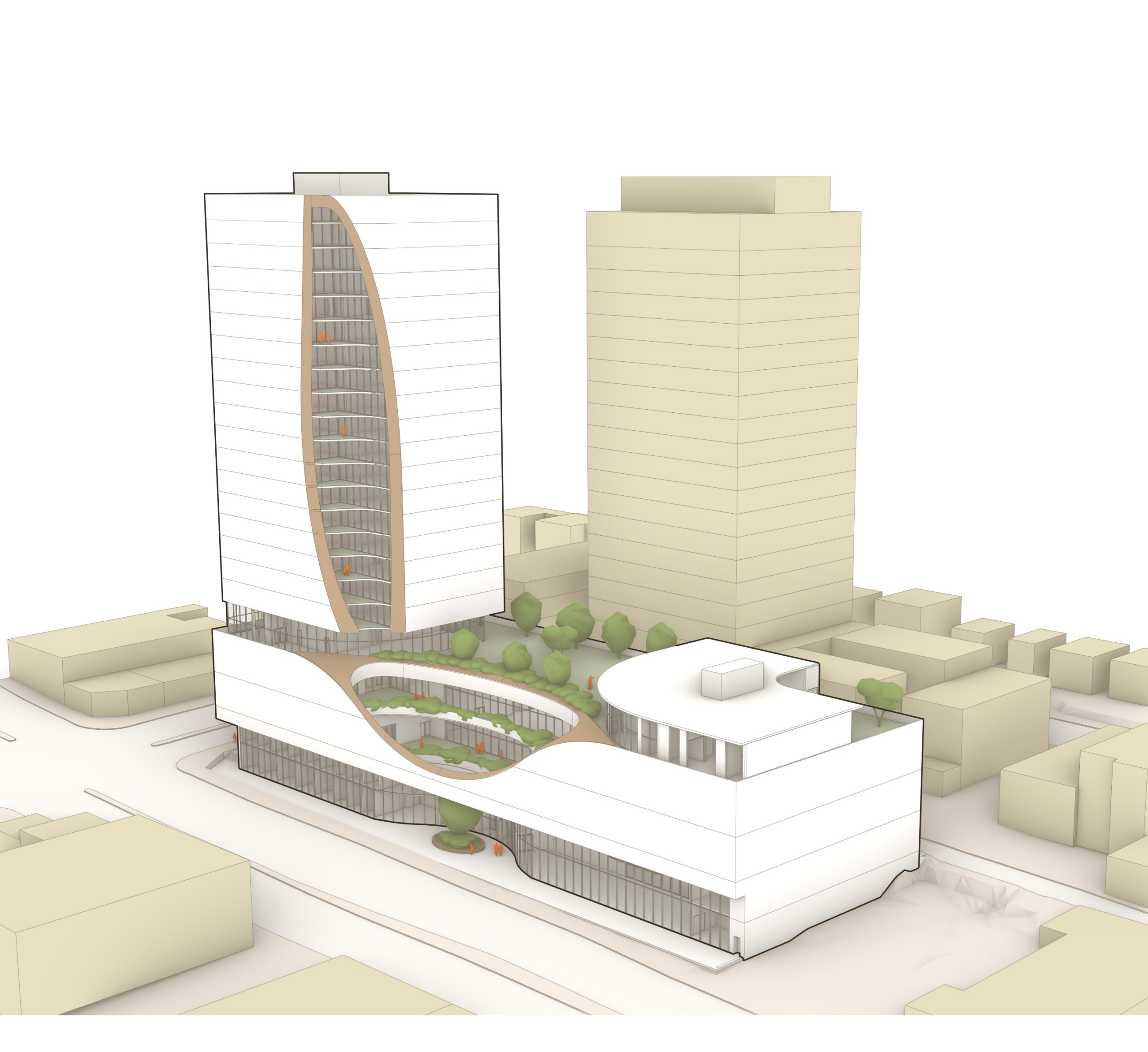

282 West 49th Avenue – Revision of Approval in Principle

Applicant: Musqueam Capital Corporation / YMCA

A minor revision to a previously approved mixed-use redevelopment of the Langara Family YMCA site, increasing total floor area to 54,300 sq. m and raising building heights by 1–2 m to accommodate design refinements. The project includes a 33-storey rental tower (306 units), a 37-storey strata tower (291 units), and an 8-storey building with 88 social housing units and a replacement YMCA community centre, at an overall FSR of 6.71.

8080 Yukon Street – Revision of Approval in Principle

Applicant: Purpose Driven Development (on behalf of Kiwanis-Soroptimist Senior Citizens Housing Society)

A minor revision to a February 2026–approved social housing project in Marpole, increasing the height of one 6-storey seniors building from 23 m to 25.3 m to accommodate new building technology. The broader project totals 903 social housing units across four buildings of up to 32 storeys, with no change to the overall floor area of 58,190 sq. m.

6212–6218 Ash Street

Applicant: 1279398 B.C. Ltd.

A proposed 6-storey mixed-use building with 30 rental units (20% below-market) and a 37-space private childcare on the ground floor, located one block from Langara–49th Avenue Station. The application increases density from 1.2 to 3.4 FSR, with a building height of 23 m.

3202–3270 Riverwalk Avenue (Parcel 11) – East Fraser Lands

Applicant: Wesgroup

An amendment to the CD-1 (499) by-law for Parcel 11 in the River District, increasing permitted height from 12 to 15 storeys (37.5 m to 48 m) to allow above-grade structured parking in response to high groundwater conditions that make deep underground excavation impractical. No change to overall floor area.

375 East 1st Avenue

Applicant: Onni

A large mixed-use development adjacent to the future Great Northern Way–Emily Carr SkyTrain Station, proposing four towers of 35–40 storeys with a total of 1,156 units (639 strata, 485 rental, and 32 artist social housing), a 225-room hotel, office and retail space, and an arts and culture production facility to be conveyed to the City. Total floor area is 110,800 sq. m with buildings reaching up to 137 m in height. Designed by Boniface Oleksiuk Politano Architects.

1045 Haro Street & 830–850 Thurlow Street

Applicant: 1045 Haro Street Limited Partnership (Chard)

Two towers of 25–26 storeys connected by an 8-storey podium in the West End, with 542 rental units (22 below-market, operated by the YWCA), a private childcare facility, and ground-floor commercial. Density increases from 6.0 to 10.6 FSR, with a building height of 80.9 m. Designed by Musson Cattell Mackey.

2406–2490 Renfrew Street & 2905–2911 East Broadway

Applicant: Easthill Development Limited Partnership

A rezoning revision for a site previously approved under CD-1 (846) in 2022, now seeking a 31-storey tower and a 6-storey mid-rise with 339 market rental units and ground-floor commercial. FSR increases from 4.1 to 7.5, with maximum height rising from 48.6 m to 97 m. Designed by Studio One Architecture.

466–476 West 27th Avenue

Applicant: Vittori Developments Ltd.

A proposed 15-storey rental building with 140 units (20% below-market) mid-block between Cambie and Yukon Streets, within 400 m of King Edward Station. The application proposes an FSR of 5.89 and a height of 45.6 m, with additional height qualifying under the Rental Development Relief Program.

365–395 West Broadway

Applicant: Bonnis Development Yukon St. Inc.

A proposed 32-storey mixed-use tower with 196 market rental units and ground-floor retail at the corner of Broadway and Yukon Street, 180 m from Broadway–City Hall Station. The application proposes an FSR of 22.0 on a 766 sq. m lot, with a building height of 104 m. Staff are supporting a height above the Broadway Plan’s standard 30-storey limit due to the site’s shallow lot depth.

1088 West 12th Avenue

Applicant: PC Urban

A proposed 26-storey mixed-use rental building in Fairview with 304 units (20% below-market) and ground-floor commercial, replacing an existing 65-unit rental building. FSR increases from 3.0 to 6.9 and height from 27.5 m to 81 m. The 26-storey height is supported under the Broadway Plan due to the site’s frontage exceeding 45.7 m. Designed by Francl Architecture.

1618–1680 East Hastings Street

Applicant: Urban Native Youth Association and City of Vancouver

An Indigenous-led mixed-use project at East Hastings and Commercial Drive proposing 157 social housing units in a 23-storey tower, with the lower four storeys housing a renewed Urban Native Youth Association centre, a Nicola Valley Institute of Technology campus, and a 44-space Indigenous childcare facility to be owned by the City. The application proposes an FSR of 5.9 and a height of 81 m.

7525 Cambie Street

Applicant: Wesgroup

A proposed 12-storey mass timber mixed-use building with 97 market rental units and ground-floor retail at the corner of Cambie and West 59th Avenue, representing the first application under the City’s Mass Timber Policy for Rezonings. FSR of 4.26 and height of 48 m. No below-market rental requirement applies, reflecting the premium cost of mass timber construction.

2611 Victoria Drive

Applicant: Vertex DC Ventures Inc. and Fastmark

A proposed 26-storey mixed-use tower with 250 rental units (20% below-market) and ground-floor commercial near Commercial–Broadway Station, at an FSR of 10.9 and a height of 83 m. Staff are recommending referral back rather than approval, as the building above the 10th storey falls within the Trout Lake public view cone (View 27.1), and the City’s view cone policy is currently under review.

807–819 Hornby Street & 908–948 Robson Street

Applicant: Reliance Properties

A proposed 35-storey mixed-use tower at the corner of Robson and Hornby Streets in Downtown Vancouver, with 176 strata units and 160 hotel rooms above an 11-storey commercial podium with ground-floor retail. The application proposes an FSR of 14.5 and a height of 108.7 m, with a negotiated cash community amenity contribution of up to $4.3 million.

David Taylor | Colliers International david.taylor@colliers.com | 604-761-7044 | vancouvermarket.ca